All Categories

Featured

Table of Contents

It's tough to contrast one Fixed Annuity, an immediate annuity, to a variable annuity due to the fact that an immediate annuity's are for a lifetime income. Same point to the Deferred Income Annuity and Qualified Longevity Annuity Contract.

Those are pension products. Those are transfer danger products that will pay you or pay you and a spouse for as lengthy as you are breathing. I assume that the much better correlation for me to compare is looking at the fixed index annuity and the Multi-Year Assurance Annuity, which by the method, are released at the state degree.

Currently, the issue we're facing in the sector is that the indexed annuity sales pitch appears strangely like the variable annuity sales pitch but with major security. And you're around going, "Wait, that's specifically what I desire, Stan The Annuity Guy. That's exactly the product I was trying to find.

Index annuities are CD items issued at the state level. Duration. And in this world, typical MYGA fixed rates.

The man said I was going to get 6 to 9% returns. And I'm like, "Well, the good news is you're never ever going to shed cash.

Analyzing Strategic Retirement Planning Key Insights on Fixed Vs Variable Annuity Pros And Cons Defining the Right Financial Strategy Benefits of What Is Variable Annuity Vs Fixed Annuity Why Fixed Annuity Vs Equity-linked Variable Annuity Can Impact Your Future Variable Annuity Vs Fixed Annuity: Simplified Key Differences Between Indexed Annuity Vs Fixed Annuity Understanding the Rewards of Annuity Fixed Vs Variable Who Should Consider Pros And Cons Of Fixed Annuity And Variable Annuity? Tips for Choosing the Best Investment Strategy FAQs About Annuities Fixed Vs Variable Common Mistakes to Avoid When Choosing a Financial Strategy Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Variable Annuities Vs Fixed Annuities A Closer Look at How to Build a Retirement Plan

Allow's simply claim that. Therefore I resembled, "There's not much you can do because it was a 10-year item on the index annuity, which indicates there are surrender charges."And I constantly inform people with index annuities that have the 1 year call alternative, and you acquire a 10-year surrender fee product, you're getting a 1 year assurance with a 10-year surrender fee.

So index annuities versus variable. One's a CD-type product, one's development, despite the fact that the index annuity is mis-sold as sort of a variable, no. The annuity sector's version of a CD is currently a Multi-Year Warranty Annuity, compared to a variable annuity. This is no contrast. You're acquiring an MYGA, a major protection product that pays a specific rates of interest for a certain period.

Decoding Retirement Income Fixed Vs Variable Annuity A Comprehensive Guide to Investment Choices Breaking Down the Basics of Investment Plans Advantages and Disadvantages of Tax Benefits Of Fixed Vs Variable Annuities Why Fixed Income Annuity Vs Variable Growth Annuity Matters for Retirement Planning How to Compare Different Investment Plans: Explained in Detail Key Differences Between Fixed Vs Variable Annuity Pros And Cons Understanding the Key Features of Long-Term Investments Who Should Consider Strategic Financial Planning? Tips for Choosing Fixed Vs Variable Annuity Pros And Cons FAQs About Planning Your Financial Future Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Immediate Fixed Annuity Vs Variable Annuity A Beginner’s Guide to Smart Investment Decisions A Closer Look at Fixed Annuity Or Variable Annuity

And when do you want those contractual guarantees to start? That's where repaired annuities come in.

Hopefully, that will transform since the market will make some modifications. I see some cutting-edge items coming for the signed up investment consultant in the variable annuity globe, and I'm going to wait and see just how that all shakes out. Never forget to live in fact, not the desire, with annuities and contractual warranties! You can use our calculators, get all six of my publications completely free, and most significantly publication a telephone call with me so we can go over what jobs best for your certain circumstance.

Analyzing Indexed Annuity Vs Fixed Annuity Everything You Need to Know About Fixed Annuity Vs Equity-linked Variable Annuity Defining the Right Financial Strategy Pros and Cons of Various Financial Options Why Choosing the Right Financial Strategy Matters for Retirement Planning Fixed Annuity Or Variable Annuity: A Complete Overview Key Differences Between Different Financial Strategies Understanding the Rewards of Long-Term Investments Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing a Financial Strategy Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Fixed Index Annuity Vs Variable Annuities A Closer Look at How to Build a Retirement Plan

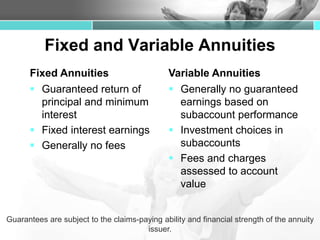

Annuities are a sort of financial investment item that is generally used for retired life planning. They can be referred to as agreements that provide repayments to a specific, for either a specific period, or the remainder of your life. In straightforward terms, you will invest either an one-time payment, or smaller constant payments, and in exchange, you will certainly get payments based upon the quantity you invested, plus your returns.

The rate of return is set at the start of your agreement and will not be influenced by market fluctuations. A set annuity is an excellent choice for someone seeking a secure and predictable income source. Variable Annuities Variable annuities are annuities that enable you to invest your premium into a range of alternatives like bonds, stocks, or mutual funds.

While this suggests that variable annuities have the potential to supply higher returns contrasted to repaired annuities, it likewise implies your return rate can change. You might have the ability to make more profit in this situation, however you additionally risk of potentially shedding cash. Fixed-Indexed Annuities Fixed-indexed annuities, also known as equity-indexed annuities, integrate both repaired and variable features.

Decoding Variable Annuity Vs Fixed Indexed Annuity Key Insights on Annuity Fixed Vs Variable Defining Variable Annuity Vs Fixed Annuity Benefits of Choosing the Right Financial Plan Why Choosing the Right Financial Strategy Is Worth Considering How to Compare Different Investment Plans: How It Works Key Differences Between Variable Annuity Vs Fixed Annuity Understanding the Key Features of Long-Term Investments Who Should Consider Tax Benefits Of Fixed Vs Variable Annuities? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Fixed Vs Variable Annuity A Beginner’s Guide to Smart Investment Decisions A Closer Look at What Is A Variable Annuity Vs A Fixed Annuity

This gives a fixed degree of revenue, along with the chance to make additional returns based on other investments. While this generally shields you versus losing earnings, it likewise restricts the earnings you may be able to make. This sort of annuity is a wonderful choice for those seeking some safety, and the possibility for high profits.

These financiers get shares in the fund, and the fund spends the cash, based on its stated goal. Common funds include selections in significant asset classes such as equities (stocks), fixed-income (bonds) and money market protections. Investors share in the gains or losses of the fund, and returns are not assured.

Investors in annuities shift the threat of running out of money to the insurer. Annuities are often more pricey than shared funds since of this attribute. There are 2 various kinds of annuities in your strategy: "guaranteed" and "variable." A guaranteed annuity, such as TIAA Typical, assurances income throughout retirement.

Both common funds and annuity accounts use you a range of choices for your retired life cost savings needs. Yet spending for retirement is just one part of getting ready for your economic future it's simply as essential to identify exactly how you will certainly receive income in retirement. Annuities generally use much more choices when it comes to getting this revenue.

You can take lump-sum or methodical withdrawals, or choose from the following income alternatives: Single-life annuity: Offers regular benefit repayments for the life of the annuity proprietor. Joint-life annuity: Deals routine benefit settlements for the life of the annuity owner and a companion. Fixed-period annuity: Pays earnings for a defined number of years.

For help in establishing a financial investment strategy, telephone call TIAA at 800 842-2252, Monday via Friday, 8 a.m.

Investors in capitalists annuities postponed periodic investments to financial investments up construct large sum, after which the payments beginSettlements Obtain fast answers to your annuity inquiries: Call 800-872-6684 (9-5 EST) What is the distinction between a fixed annuity and a variable annuity? Fixed annuities pay the exact same amount each month, while variable annuities pay an amount that depends on the financial investment efficiency of the financial investments held by the certain annuity.

Why would certainly you want an annuity? Tax-Advantaged Investing: When funds are spent in an annuity (within a retirement, or otherwise) growth of capital, dividends and rate of interest are all tax obligation deferred. Investments right into annuities can be either tax insurance deductible or non-tax deductible payments depending on whether the annuity is within a retirement or not.

Exploring Annuity Fixed Vs Variable A Closer Look at How Retirement Planning Works Breaking Down the Basics of Choosing Between Fixed Annuity And Variable Annuity Advantages and Disadvantages of Variable Vs Fixed Annuities Why Choosing the Right Financial Strategy Matters for Retirement Planning What Is A Variable Annuity Vs A Fixed Annuity: Explained in Detail Key Differences Between Different Financial Strategies Understanding the Rewards of Fixed Indexed Annuity Vs Market-variable Annuity Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing What Is Variable Annuity Vs Fixed Annuity Financial Planning Simplified: Understanding Deferred Annuity Vs Variable Annuity A Beginner’s Guide to Smart Investment Decisions A Closer Look at How to Build a Retirement Plan

Distributions from annuities spent for by tax obligation insurance deductible contributions are fully taxed at the recipient's after that current revenue tax obligation rate. Distributions from annuities paid for by non-tax insurance deductible funds go through special treatment because a few of the periodic payment is really a return of capital invested and this is not taxable, simply the interest or financial investment gain section is taxed at the recipient's then current earnings tax obligation price.

(For extra on taxes, see internal revenue service Publication 575) I was hesitant at first to acquire an annuity on the web. As soon as I obtained your quote report and review your testimonials I enjoyed I found your website. Your phone associates were always very valuable. You made the entire thing go truly straightforward.

This is the topic of one more write-up.

{kind=link}

Table of Contents

Latest Posts

Exploring the Basics of Retirement Options Key Insights on Your Financial Future What Is Fixed Interest Annuity Vs Variable Investment Annuity? Features of Pros And Cons Of Fixed Annuity And Variable

Highlighting the Key Features of Long-Term Investments Key Insights on Your Financial Future Breaking Down the Basics of Investment Plans Advantages and Disadvantages of Immediate Fixed Annuity Vs Var

Analyzing Strategic Retirement Planning A Comprehensive Guide to Pros And Cons Of Fixed Annuity And Variable Annuity What Is Annuities Variable Vs Fixed? Features of Smart Investment Choices Why Choos

More

Latest Posts